The SACCO Societies Regulatory Authority (SASRA) has raised concern over the ever‑increasing concentration of assets within Kenya’s regulated SACCO industry, warning that a small cluster of large institutions continues to dominate the sector.

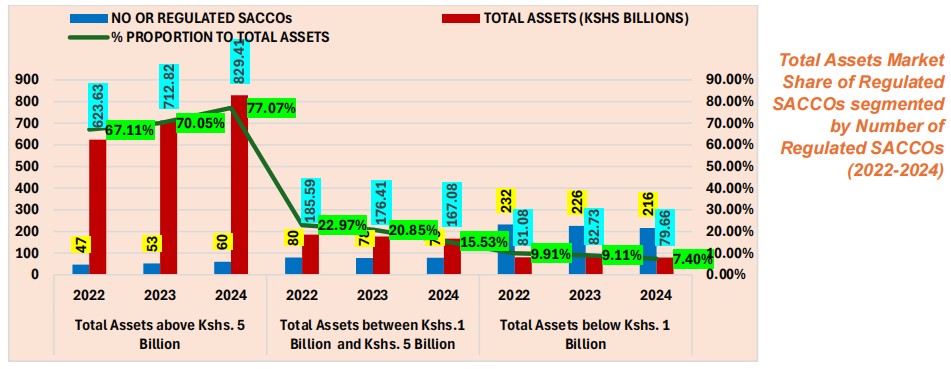

According to SASRA, by 2024, a total of 60 large‑tiered regulated SACCOs controlled 77.07 per cent of the industry’s total assets, amounting to KSh 829.41 billion. This left the remaining 295 mid‑ and small‑tiered SACCOs to share just 22.93 per cent of the assets, underscoring the widening gap between the largest players and smaller cooperatives.

In his submission in the SACCO Supervision Annual Report, 2024, SASRA Acting CEO David Sandagi noted that while asset concentration allows the Authority to deploy supervisory resources more efficiently under its risk‑based framework, it also presents challenges.

“The very many small‑sized regulated SACCOs are unable to generate sufficient revenues from their relatively small asset base to meet operational needs, ward off competition, and cater for compliance costs,” he said.

Similar risks remain evident in deposit distribution. Forty large‑tiered SACCOs controlled 65.83 per cent of the industry’s total deposits, while 69 mid‑tier SACCOs held 23.20 per cent. The remaining 246 small‑tiered SACCOs shared just 10.97 per cent of deposit liabilities, highlighting the structural imbalance across the cooperative movement.

Sandagi emphasised that financial stability and soundness remain the fulcrum of SASRA’s supervisory activities, noting that the deposit‑taking SACCO (DT‑SACCO) segment continues to dominate the industry, controlling over 80 per cent of total assets, deposits, and loans. He reported that DT‑SACCOs registered increased capitalization in all key adequacy ratios. The capital‑to‑total assets ratio rose to 17.28 per cent in 2024, above the prescribed minimum of 10 per cent, compared to 16.07 per cent in 2023. Institutional capital to total assets also improved to 11.97 per cent against the minimum of 8 per cent, up from 9.11 per cent the previous year.

ALSO READ:

SASRA warns of fragile SACCO funding structure as wealthy savers dominate majority deposits

The non‑withdrawable deposit‑taking (NWDT) SACCO segment also recorded gains as their aggregate core capital to total assets ratio increased to 10.87 per cent in 2024, above the minimum 8 per cent, compared to 10.40 per cent in 2023. Core capital to total deposits rose to 14.26 per cent, well above the 5 per cent minimum, up from 13.51 per cent in 2023. Retained earnings and disclosed reserves to core capital climbed to 66.89 per cent in 2024 from 62.49 per cent in 2023, surpassing the required 50 per cent threshold.

Sandagi explained that these improvements reflect regulatory pressure and advocacy for increased retention, ensuring that institutional capital forms the bulk of SACCOs’ core capital rather than share capital, which is often more expensive. He stressed that while the sector’s resilience is evident, the imbalance between large and small SACCOs remains a pressing concern requiring sustained oversight.

By Masaki Enock

Get more stories from our website: Sacco Review.

For comments and clarifications, write to: Saccoreview@

Kindly follow us via our social media pages on Facebook: Sacco Review Newspaper for timely updates

Stay ahead of the pack! Grab the latest Sacco Review newspaper!